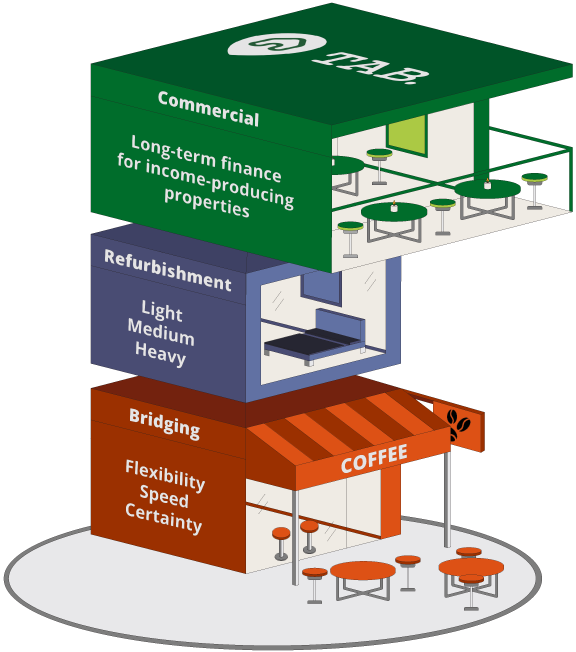

Commercial bridging finance

TAB’s second charge commercial loans are secured against UK commercial properties. Second charge loans allow you to borrow money on a second charge legal basis. This means that you can take another loan out on a property providing there is enough equity to pay your existing first charge, and the second charge loan. Second charge loans are often used for the redevelopment of existing properties, the purchase of an investment property or even business expansion.

Our experience means we can be flexible with our valuations and consider projects that more traditional lenders would not. We pride ourselves on trust and transparency. TAB lends directly to borrowers and through intermediaries. We offer loans up to 70% of the valuation of your project, including the cost of borrowing.

TAB loans are unregulated. Any property used as security is at risk of repossession if you do not keep up with your payments.

Second charge commercial loan product details

Other charges may apply

Related products

How it works

Borrower applies

Following an initial enquiry, borrowers apply for a loan through our application process.

Decision made

Our team undertakes their due diligence and underwriting process on the borrower and the security property. Terms are then agreed.

Perfect match

The loan is then matched with investors on the TAB platform. Funds are typically available within just 14 days.